Recently, I see a lot of comments (or rather, cursing) on online forums and Facebook regarding the recent raise in the CPF Minimum Sum for Retirement Account and Medisave Account (See CPF news release by clicking here). Opinions are divided whether CPF is good for a Singaporean or Singapore Permanent Resident, but if you own a pink or blue IC, you have no choice but to follow.

So, this prompted me to do some excel sheet and run some numbers. Here are some assumptions that I’m going to make for this imaginary person :

– Starting work in 2014 at the age of 25.

– Starting salary of SGD3,000 per month (which happens to be the median gross salary in 2012 on MOM’s website – link), annual increment of 5% until reaching its peak at SGD10,000 per month (age 50) , and 3 months of bonus (including AWS) every year.

– Current CPF contribution rates (Link) remains unchanged

– Purchase a HDB flat valued at SGD500,000 and share the payment with the spouse at the age of 30. Pay 20% deposit (5% cash, 15% CPF-OA) and take a loan for the remainder 80% (30 years @ 2.6% interest). This workout to a CPF-OA down-payment of SGD37,500 and monthly installment of SGD800 from this person’s CPF-OA.

– Purchase private integrated medical shield plan with Medisave. I used Preferred plan from NTUC INCOME (Link)

– CPF-OA interest of 2.5% and 4% for CPF-SA and Medisave

– CPF Retirement Account Minimum Sum amount to increase at 6.21% per annum (2003-2014 average) and CPF Medisave Minimum Sum amount to increase at 5.19% per annum (2003-2014 average).

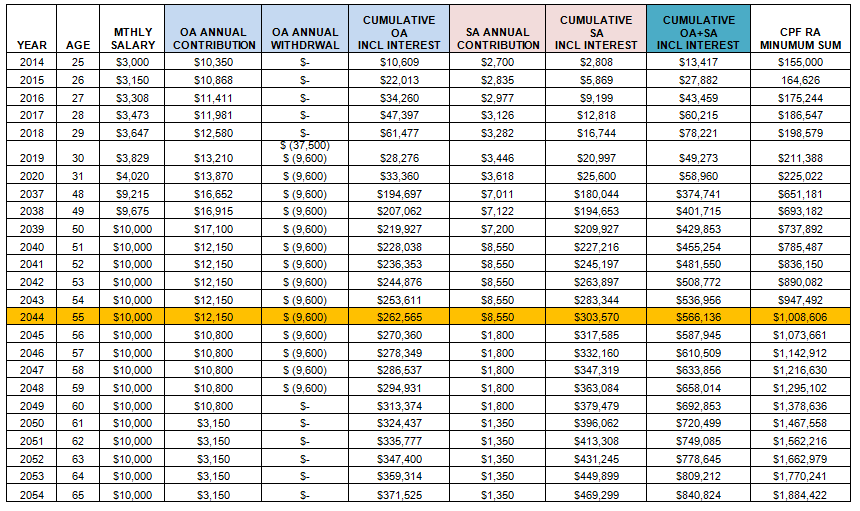

Analysis (Retirement Account)

Minimum Sum in 2044 would have reached the magical sum of SGD 1 million and cumulative OA+SA would be SGD 566,000, half the projected Minimum Sum required. One would need to pledge his/her property to meet the Minimum Sum, which I think need to be worth SGD 1 million in 2044, bearing in mind that he/she is still servicing the loan and the amount pledged would then be lower.

My conclusion is that our current CPF contribution would never be enough to meet the Minimum Sum based on current rate of increase.

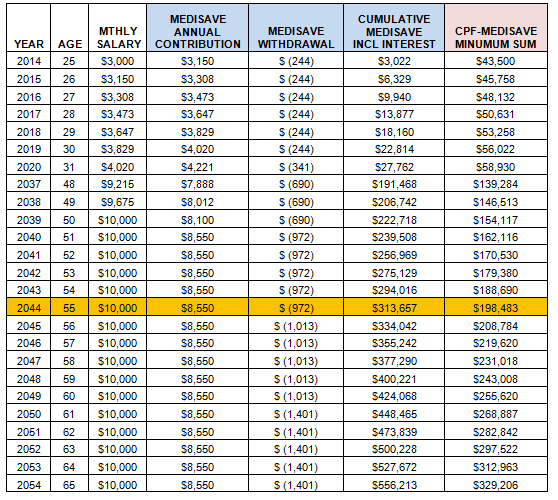

Analysis (Medisave Account)

Minimum Sum for Medisave Account in 2044 would be SGD 192,000 and cumulative OA+SA would be SGD 313,000. On paper, it may look enough, but this does not include any accidental medical fees one has to pay for hospitalization (no shield rider).

My personal conclusion is that the rate of increase in Minimum Sum for Retirement Account is definitely not sustainable and all Singaporeans/ PRs will never have enough money in their Retirement Account when they reach 55. Furthermore, the scheme is heavily reliant on property value. If there’s a property crash, most people will be badly affected.

While it seems like the Minimum Sum for Medisave Account looks attainable, there are many unforeseen circumstances which may result in hospitalization. Hence, I feel its very important to get a private integrated shield plan and a rider to cover any deductibles and co-payment.

I believe what the CPF Minimum Sum scheme is to allow Singaporeans/PRs to have at least some money for their retirement, but its definitely not enough. The more important action is how one handles their cash and what they do to ensure that they have enough money for their retirement. What financial planning have you done to ensure that you have enough for your retirement, and at the same time, save up for your children so that they have a head-start?

Leave a comment